Facultad de Ciencias Contables, Vol. 4, 2025, elocation-id: eamr.v4a07.2025 | ISSN-e: 2805-8658

Artículo original de investigación

Macroeconomic resilience and the Debt-Investment Nexus in Zambia: empirical insights for sustainable growth

Resiliencia macroeconómica y el nexo deuda-inversión en Zambia: perspectivas empíricas para el crecimiento sostenible

Tryson Yangailo1

https://orcid.org/0000-0002-0690-9747

https://doi.org/10.22209/amr.v4a07.2025

elocation-id: eamr.v4a07.2025

Recibido: julio 2025.

Aceptado: diciembre 2025.

Cómo citar: Yangailo, T. (2025). Macroeconomic resilience and the Debt-Investment Nexus in Zambia: empirical insights for sustainable growth. Accounting and Management Research, 4, eamr.v4a07.2025. https://doi.org/10.22209/amr.v4a07.2025

Abstract

This study provides a thorough quantitative analysis of Zambia’s macroeconomic performance from 2010 to 2023. It focuses on the relationship between external debt, inflation, investment, and economic growth. The study uses time-series data mainly from the World Bank and advanced econometric techniques in Jamovi and RStudio to investigate the determinants of GDP growth and debt sustainability. Descriptive statistics reveal persistently high and volatile inflation averaging 10.51%, moderate yet unstable GDP growth averaging 4.49%, and significant external debt stress, evidenced by an average debt-to-GNI ratio of 69.77%. Correlation analysis indicates a strong negative relationship between external debt and GDP growth (r = -0.705, p = 0.005) and a negative correlation between foreign direct investment (FDI) and external debt (r = -0.539, p = 0.047). This suggests the crowding-out effect of debt on investment. Regression models further substantiate these relationships. External debt has a negative effect on GDP growth, which is statistically significant (coefficient = -0.0405, p = 0.032). This confirms the debt overhang hypothesis. Additionally, external debt significantly increases debt servicing obligations as a percentage of both GNI (coefficient = 0.05875, p = 0.003) and exports (coefficient = 0.1292, p = 0.015). This underscores Zambia’s vulnerability to debt burdens and trade shocks. However, foreign direct investment (FDI) alone does not mitigate debt servicing pressures. Moderation analysis reveals that the positive impact of FDI on growth diminishes as debt levels rise, resulting in a significant negative interaction effect (coefficient = -0.00936, p = 0.042). This finding underscores the conditional effectiveness of FDI in high-debt environments. The study identifies inflation, inefficient public investment, and high external debt as challenges that reinforce each other and undermine Zambia’s economic resilience and sustainable growth. Theoretical implications validate well-established economic concepts, such as debt overhang, crowding-out, and the conditional nature of foreign direct investment (FDI) benefits. Practical recommendations emphasize debt restructuring, inflation stabilization, public investment reform, export diversification, and institutional capacity building. Ultimately, this study provides policymakers with an evidence-based roadmap for overcoming Zambia’s macroeconomic vulnerabilities and promoting inclusive, long-term development.

Keywords: Inflation, External Debt, Foreign Direct Investment, Economic Diversification, Economic Resilience

JEL: E31; F21; H63; O23; O55

Resumen

Este estudio proporciona un análisis cuantitativo exhaustivo del desempeño macroeconómico de Zambia entre 2010 y 2023. Se centra en la relación entre la deuda externa, la inflación, la inversión y el crecimiento económico. El estudio utiliza datos de series temporales, principalmente del Banco Mundial, y técnicas econométricas avanzadas en Jamovi y RStudio para investigar los determinantes del crecimiento del PIB y la sostenibilidad de la deuda. Las estadísticas descriptivas revelan una inflación persistentemente alta y volátil, con un promedio del 10,51%, un crecimiento del PIB moderado pero inestable, con un promedio del 4,49%, y una importante tensión en la deuda externa, evidenciada por una relación deuda/INB promedio del 69,77%. El análisis de correlación indica una fuerte relación negativa entre la deuda externa y el crecimiento del PIB (r = -0,705, p = 0,005) y una correlación negativa entre la inversión extranjera directa (IED) y la deuda externa (r = -0,539, p = 0,047). Esto sugiere el efecto de desplazamiento de la deuda sobre la inversión. Los modelos de regresión corroboran estas relaciones. La deuda externa tiene un efecto negativo en el crecimiento del PIB, estadísticamente significativo (coeficiente = -0,0405, p = 0,032). Esto confirma la hipótesis del exceso de deuda. Además, la deuda externa incrementa significativamente las obligaciones de servicio de la deuda como porcentaje tanto del INB (coeficiente = 0,05875, p = 0,003) como de las exportaciones (coeficiente = 0,1292, p = 0,015). Esto subraya la vulnerabilidad de Zambia a las cargas de deuda y a las perturbaciones comerciales. Sin embargo, la inversión extranjera directa (IED) por sí sola no mitiga las presiones del servicio de la deuda. El análisis de moderación revela que el impacto positivo de la IED en el crecimiento disminuye a medida que aumentan los niveles de deuda, lo que resulta en un efecto de interacción negativo significativo (coeficiente = -0,00936, p = 0,042). Este hallazgo subraya la efectividad condicional de la IED en entornos de alta deuda. El estudio identifica la inflación, la ineficiencia de la inversión pública y la elevada deuda externa como desafíos que se refuerzan mutuamente y socavan la resiliencia económica y el crecimiento sostenible de Zambia. Las implicaciones teóricas validan conceptos económicos bien establecidos, como el exceso de deuda, el efecto desplazamiento y la naturaleza condicional de los beneficios de la inversión extranjera directa (IED). Las recomendaciones prácticas enfatizan la reestructuración de la deuda, la estabilización de la inflación, la reforma de la inversión pública, la diversificación de las exportaciones y el fortalecimiento de la capacidad institucional. En definitiva, este estudio proporciona a los responsables políticos una hoja de ruta basada en la evidencia para superar las vulnerabilidades macroeconómicas de Zambia y promover un desarrollo inclusivo a largo plazo.

Palabras clave: inflación, deuda externa, inversión extranjera directa, diversificación económica, resiliencia económica.

Introduction

Zambia’s economic trajectory has experienced both periods of prosperity and depression due to a confluence of internal and external causes. Due to its reliance on copper exports, Zambia’s economy is vulnerable to shocks and fluctuations in global commodity prices (Nel et al., 2017). Despite Zambia’s substantial copper reserves, the country continues to struggle with macroeconomic issues such as rising inflation, increasing external debt, and unpredictable foreign direct investment (FDI) inflows, which have stunted long-term growth and caused volatility in the economy. Achieving sustainable economic growth remains difficult due to the interplay of numerous macroeconomic factors, although the government has implemented several policy initiatives to address these issues.

A key element of sustainable development is economic resilience, or a nation’s ability to withstand and recover from economic shocks (Nel et al., 2017). This study examines how Zambia’s economic vulnerabilities affect its ability to encourage investment, maintain fiscal stability, and promote economic expansion. By analyzing regional and international research and applying relevant economic theories, this study aims to provide insights into possible strategies to improve Zambia’s stability and resilience.

Several macroeconomic variables, including investment flows, inflation, and debt sustainability, affect economic resilience in emerging markets. Zambia’s economic performance and vulnerabilities are clarified through theoretical frameworks on inflation, debt, and investment.

There is much debate in the economic literature about the relationship between GDP growth and inflation. While high inflation reduces purchasing power, destabilizes financial markets, and increases borrowing costs, moderate inflation can stimulate economic activity according to classical and Keynesian economic theories (Girdzijauskas et al., 2022; Muhammad, 2023). Empirical research suggests that supply-side constraints, exchange rate volatility, and fiscal imbalances are often at the root of inflationary pressures in developing countries (Silvia et al., 2023). Through monetary intervention, central bank policy plays a crucial role in reducing inflationary fears (Jackson, 2024). The threshold effect of inflation is demonstrated by Sani et al. (2024), who show that excessive inflation (above 10%) is detrimental to GDP growth, while moderate inflation is conducive to growth. These results highlight the importance of countercyclical fiscal policies and inflation targeting frameworks in maintaining economic stability.

The debt overhang idea suggests that excessive external debt hampers economic growth by reducing the fiscal capacity for profitable investment (Mammadli et al., 2021). Research on emerging markets suggests that high debt levels lead to slower GDP growth by crowding out both public and private investment (Hilton, 2021; Manasseh et al., 2022). Zambia’s growing external debt burden has reduced government spending and diverted funds away from infrastructure, health, and education (Sundus et al., 2022; Iqbal et al., 2023). Debtor countries have been able to restore economic stability through prudent fiscal management and debt restructuring (Oyadeyi et al., 2024). Institutional structure and quality of governance are critical in mitigating the negative impact of debt on growth (Yangailo, 2024a).

Foreign direct investment is believed to promote economic growth through capital accumulation, job creation, and knowledge transfer (Yangailo, 2024b; Zekarias, 2016). However, its effectiveness depends on macroeconomic stability, quality of governance, and institutional framework (Ndlovu and Haabazoka, 2024). Research shows that countries with high debt levels often struggle to attract and retain foreign direct investment due to perceived risks (Ndaba, 2015). Effective investment allocation is necessary to maximize the economic benefits of capital production, which is essential for sustainable growth. In countries that rely heavily on natural resources, weak institutional frameworks can hinder investment efficiency and economic diversification (Claudio-Quiroga et al., 2022).

Comparisons of macroeconomic stability provide important insights into the most effective ways to manage inflation, debt, and investment. Research on emerging markets shows that monetary and fiscal policies are critical to reducing economic vulnerabilities (Pegkas, 2015; Nistor, 2014). Countries that have effectively controlled inflation and ensured debt sustainability have done so through sound economic policies, diversification initiatives, and institutional reforms (El-Mahdy and Torayeh, 2009; El Aboudi and Khanchaoui, 2021).

Excessive external debt has a significant impact on economic resilience. Research shows that high debt reduces government investment, undermines investor confidence, and increases a country’s vulnerability to external shocks (Harmon, 2012; Osewe, 2017). The relationship between debt and resilience is influenced by export earnings, exchange rate stability, and fiscal policy. Zambia’s dependence on copper exports has increased its economic vulnerability, as falling global copper prices have increased the risk of a financial crisis (Nel et al., 2017).

Research suggests that resource-dependent economies should prioritize investment efficiency. Building infrastructure, establishing public-private partnerships, and allocating funds efficiently are essential to promoting economic resilience (Zekarias, 2016). However, investment efficiency is often hampered by governance issues, ineffective project management, and a lack of economic diversification (Ndaba, 2015). The need for diversified investment options is highlighted by Zambia’s over-reliance on mining-centric foreign direct investment, which has hindered inclusive economic development (Yangailo, 2024b).

The main objective of this study was to analyze Zambia’s inflation, public debt, foreign direct investment (FDI), and economic diversification in order to recommend policies that would enhance economic resilience and promote long-term growth.

This study primarily aimed to evaluate the impact of external debt, inflation, and investment on Zambia’s economic growth and debt sustainability from 2010 to 2023. The study analyzed key macroeconomic trends, such as inflation, gross domestic product (GDP) growth, foreign direct investment (FDI), external debt, and debt servicing. Using regression models, the study examined the structural relationships between external debt, investment, inflation, and GDP growth to determine their influence on the country’s economic trajectory. Additionally, the study examined debt sustainability by evaluating the impact of external debt on debt service obligations as a percentage of gross national income (GNI) and export earnings. Additionally, the study investigated the moderating role of external debt in the relationship between foreign direct investment (FDI) and GDP growth, highlighting how debt dynamics may alter the developmental benefits of investment inflows.

Literature Review

Regional Economic Resilience

Nel et al. (2017) study the resilience of Zambia’s Copperbelt to economic shocks, highlighting the differences between formal and informal economic resilience systems. Their findings draw attention to structural inequalities by showing that while foreign investment has supported the formal mining industry, the broader population has turned to illicit economic activities. This is consistent with broader concerns about the viability of economies in resource-dependent regions, where changes in commodity prices exacerbate economic volatility.

Inflation and Economic Growth

The effect of inflation on economic outcomes has been the subject of numerous studies. Girdzijauskas et al. (2022) present a unique model that considers economic bubbles and their macroeconomic effects, arguing that unemployment and inflation are essential components of sustainable economic growth. Muhammad (2023) provides empirical evidence that inflation has a positive and statistically significant impact on economic growth, underscoring the need for effective inflation control strategies. The relationship between inflation and growth is emphasized by Silvia et al. (2023), who argue that dynamic control of inflation through fiscal and monetary policies is essential for its management. To quantify the dynamics of inflation, Jackson (2024) provides mathematical models such as the Phillips curve and the Fisher equation. Building on previous hypotheses, Sani et al. (2024) analyze pan-panel data from 1990 to 2021 across several countries and find a statistically significant negative association between high inflation (above 10%) and GDP growth. Their results illustrate the threshold effect of inflation, suggesting that high inflation discourages investment and increases unemployment, while moderate inflation can stimulate economic activity.To maintain economic stability, the study highlights the importance of structural adjustment, countercyclical fiscal policies, and inflation targeting frameworks.

Public Debt and Economic Stability

The relationship between public debt and economic expansion has been much debated. Mammadli et al. (2021) argue that economic performance, resource endowment, and external borrowing conditions are important determinants of public debt accumulation. According to Hilton (2021), Ghana’s public debt is not strongly correlated with GDP growth in the short run but is a significant predictor of economic performance in the long run. According to Manasseh et al. (2022), governance elements significantly mitigate the negative impact of external debt on sub-Saharan African economies. Similar conclusions are supported by Sundus et al. (2022) in the case of Pakistan, where growing debt constraints are exacerbated by fiscal deficits and currency depreciation. In the context of Pakistan, Iqbal et al. (2023) provide evidence in support of these claims, showing a remarkable inverse relationship between GDP growth and historical rates of debt service and inflation. Using advanced econometric models, the study highlights the need for sustainable debt management strategies to reduce long-term economic instability.

Debt Sustainability and Governance

Debt sustainability remains a major concern, particularly in emerging markets. According to an assessment of Nigeria’s debt sustainability by Oyadeyi et al. (2024), only internal debt is sustainable in the medium and long term, while total and external debt are above sustainable levels. Sharaf and Shahen (2023) examine the relationship between inflation and Sudan’s external debt and show how nonlinear dynamics affect inflation outcomes. After a comprehensive review of the literature, Yangailo (2024a) concludes that different countries have different thresholds for debt growth, highlighting the importance of public confidence and governance in debt policy. Harmon (2012) examines Kenya’s debt dynamics and finds a modest positive correlation between public debt and GDP growth and a strong negative correlation with interest rates. To ensure a stable debt trajectory, El-Mahdy and Torayeh (2009) assess Egypt’s debt sustainability and argue for fiscal reform. Similar issues are raised in the Kenyan context by Osewe (2017), who finds that while inflation and external debt are related, there is little evidence that they have a direct impact on GDP growth. This suggests that while there may be a link between debt and inflationary pressures, debt is usually not the main driver of short-term changes in the economy. As both high and low inflation affect loan repayment and the competitiveness of SMEs, El Aboudi and Khanchaoui (2021) also highlight the Moroccan situation and emphasize the need for a balanced inflation policy. In their assessment of the current debt sustainability framework, Arnone et al. (2008) argue that long-term economic stability requires a comprehensive strategy that addresses both external and domestic debt within a constrained government budget.

Foreign Direct Investment and Economic Growth

Although the impact of foreign direct investment (FDI) varies from situation to situation, it is generally accepted that FDI stimulates economic growth. According to Yangailo (2024b), exports and gross national income (GNI) per capita have a greater impact on Zambia’s economic growth than FDI. According to Ndlovu and Haabazoka (2024), FDI lowers inflation in Zambia but has no effect on interest rates or unemployment. Zekarias (2016) argues for better regional cooperation and an investment-friendly environment, while highlighting the positive correlation between FDI and economic growth in East Africa. Ndaba (2015) argues that inclusive economic development has been hampered by Zambia’s overdependence on FDI, which is concentrated in the mining sector.

Global and Regional Perspectives on FDI

Zekarias (2016) examined 34 years of foreign direct investment inflows to 14 East African countries and found a positive correlation between FDI and economic growth. The report suggested improving human capital, strengthening regional cooperation, and improving the investment climate to optimize the benefits of FDI. Claudio-Quiroga et al. (2022) examined the impact of Chinese FDI in five African countries and found a statistically significant effect in Nigeria, but mixed results in South Africa and Kenya. These results highlight the need for FDI plans that are country-specific and adapted to different economic conditions.

Additional information on the relationship between economic growth and FDI can be found in international research. Pegkas (2015) examined this dynamic in the euro area between 2002 and 2012, finding a positive correlation between GDP growth and FDI in the long run. After analyzing Romania’s economic performance, Nistor (2014) concluded that FDI inflows boost economic growth, but the magnitude of this effect varies depending on domestic conditions.

Literature and Knowledge Gaps

This study makes a significant contribution to the existing literature by addressing critical gaps with an integrated analysis of inflation, external debt, foreign direct investment (FDI), and economic growth within a unified framework. While prior research has primarily examined these macroeconomic variables in isolation, this study synthesizes them to reveal their collective impact on Zambia’s economic resilience and debt sustainability. In doing so, the study provides a more comprehensive understanding of the structural challenges faced by resource-dependent economies, especially those dealing with the complex dynamics of external borrowing and fluctuating investment inflows.

From a methodological standpoint, the research employs a rigorous, multifaceted approach that incorporates moderation analysis, multivariate regression, and correlation techniques. This analytical design allows for the examination of conditional relationships and interdependencies that were often overlooked in previous studies. By clarifying these relationships, the study resolves inconsistencies in previous research and establishes a stronger basis for formulating macroeconomic policies in low- and middle-income countries.

Overall, the study provides a cohesive, empirically grounded perspective on the relationship between public debt, inflation, foreign direct investment (FDI), and economic growth. Beyond advancing academic inquiry, the study provides practical insights for redefining the policy agenda on economic resilience and debt sustainability in structurally constrained and externally vulnerable economies.

Methodology

This study takes a quantitative approach to research, using macroeconomic time-series data from 2010 to 2023 to evaluate how external debt, inflation, and investment affect Zambia’s economic growth and debt sustainability. The data were primarily sourced from the World Bank’s World Development Indicators (WDI) and, when available, cross-verified with national sources (Bank of Zambia,2025). The analysis was performed using Jamovi, a user-friendly statistical platform that integrates R syntax for advanced procedures. RStudio was used for deeper econometric modeling and code-based analysis, particularly for diagnostics and interaction effects.

The methodology proceeds through several empirical steps. First, descriptive statistics are computed to provide an overview of key variables including GDP growth (annual percentage), gross fixed capital formation (percentage of GDP), inflation (percentage), foreign direct investment (FDI, percentage of GDP), external debt (percentage of GNI), and debt servicing obligations (percentage of GNI and percentage of exports). This stage reveals trends, volatility, and central tendencies in Zambia’s macroeconomic profile.

Next, stationarity tests are conducted using the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) methods to determine if the variables are suitable for regression analysis or if differencing is required. The results confirmed that most of the variables were stationary at their initial levels or after first differencing, which ensures the robustness of the regression estimates.

Third, a correlation analysis was performed to explore bivariate relationships among the variables, particularly between GDP growth, external debt, foreign direct investment (FDI), and investment. This analysis provides insight into the expected signs and strength of the subsequent regression coefficients. Fourth, the study estimated three key multiple regression models to quantify the structural relationships of interest.

Model 1: Determinants of GDP Growth

GDP Growth = β₀ + β₁(Gross Fixed Capital Formation) + β₂(External Debt) + β₃(Inflation) + ϵ

Model 2: Debt Service (% of GNI)

Debt Service (% of GNI) = β₀ + β₁(External Debt Stocks) + β₂(FDI) + ϵ

Model 3: Determinants of Debt Service (% of Exports)

Debt Service (% of Exports) = β₀ + β₁(External Debt Stocks) + ϵ

Finally, a moderation analysis was conducted in RStudio using interaction terms to test whether the impact of foreign direct investment (FDI) on gross domestic product (GDP) growth depends on the level of external debt.

This rigorous, multilayered methodological design, grounded in robust econometric techniques and employing both Jamovi and RStudio, provides deep insights into Zambia’s debt-growth dynamics and offers a strong evidence base for future macroeconomic policy decisions.

Ethical Considerations

This study adhered to ethical research standards. To avoid misrepresentation or overgeneralization, all data sources were appropriately cited and the results were presented in an open and honest manner.

Results

This study provides an in-depth, analytical review of Zambia’s macroeconomic performance. It focuses on key indicators, including inflation, gross domestic product (GDP) growth, foreign direct investment (FDI), gross fixed capital formation, external debt, and debt servicing obligations. Integrating descriptive statistics, correlation analysis, stationarity tests, regression models, and moderation analysis provides a comprehensive understanding of the dynamics that shape Zambia’s economic stability and growth prospects.

The descriptive statistics reveal the challenging inflation environment that Zambia has experienced, characterized by an average inflation rate of 10.51% and significant volatility (standard deviation = 4.78%). The inflation rate fluctuated significantly, ranging from a minimum of 6.43% to a maximum of 22.02%, with a median of 8.83%. These fluctuations suggest episodes of price instability likely driven by external shocks, exchange rate pressures, and fiscal imbalances. These findings corroborate the work of Mwamba and Simutanyi (2019), who also documented inflation volatility in Zambia linked to external commodity shocks. However, unlike Botswana, which experienced relatively stable inflation rates during the same period (Chanda, 2017), Zambia’s inflation was more sensitive to fiscal deficits and exchange rate depreciation. Persistent inflation at these levels tends to erode real incomes and purchasing power, necessitating tighter monetary policies to restore price stability.

Descriptive Analysis

Table 1 presents descriptive information on Zambia’s main macroeconomic variables during the period under review. Zambia’s inflation rate was 10.51%, with a median of 8.83%, according to consumer prices. The standard deviation of 4.78%, which indicates significant variability, indicates that inflation ranged from a low of 6.429% to a high of 22.02%. The data suggest that Zambia has experienced periods of excessive inflation, which could threaten the country’s economic stability and reduce the purchasing power of its citizens. If inflationary pressures persist, tight monetary policy may be required. Zambia’s economy is performing well overall, with a median GDP growth rate of 4.88% and an average of 4.49%. The standard deviation of 2.98% indicates volatility, as GDP growth rates range from a low of -2.785% to a high of 10.30%. These developments demonstrate Zambia’s economic resilience, as the country has successfully rebounded from periods of low growth to robust recovery.

Table 1: Descriptive Statistics of Key Macroeconomic Indicators

|

Mean |

Median |

SD |

Minimum |

Maximum |

|

|---|---|---|---|---|---|

|

Inflation, consumer prices (annual %) |

10.51 |

8.83 |

4.78 |

6.429 |

22.02 |

|

GDP growth (annual %) |

4.49 |

4.88 |

2.98 |

-2.785 |

10.30 |

|

Foreign direct investment, net inflows (% of GDP) |

3.94 |

3.72 |

2.88 |

-0.223 |

8.53 |

|

Gross fixed capital formation (% of GDP) |

30.64 |

29.17 |

5.26 |

23.878 |

38.81 |

|

External debt stocks (% of GNI) |

69.77 |

68.48 |

50.05 |

0.000 |

168.40 |

|

Total debt service (% of GNI) |

4.48 |

3.64 |

3.80 |

0.826 |

11.97 |

The average ratio of net FDI inflows to GDP was 3.94%, with a median of 3.72%. With a standard deviation of 2.88% and a range of -0.223% to 8.53%. Disinvestment is indicated by periods of negative FDI inflows, which could be caused by external economic shocks, regulatory challenges, or domestic macroeconomic instability. These examples highlight the importance for Zambia of maintaining a stable and attractive business environment to attract FDI, which is essential for economic growth and job creation. Gross fixed capital formation, a key measure of investment in physical assets, averaged 30.64% of GDP with a median of 29.17%. A range of 23.878% to 38.81% with a standard deviation of 5.26% indicates a sustained effort to improve infrastructure and productive capacity. Long-term economic growth depends on high levels of gross fixed capital formation as it promotes the development of new industries, technological advances, and improved public services. However, sustaining such levels of investment requires efficient resource allocation and a favorable policy climate.

Table 1 shows that Zambia’s external debt stock has a median of 68.48% and an average of 69.77% of GNI. Significant volatility is indicated by the standard deviation of 50.05% and the wide range of 0% to 168.40%, which could be caused by changes in borrowing cycles, external financing conditions, or debt restructuring initiatives (Liu, Savastano, & Zettelmeyer 2020; Panizza, Sturzenegger & Zettelmeyer 2009; Reinhart & Rogoff, 2009). Fiscal sustainability may be threatened by high debt levels, especially if debt service payments consume a significant share of government revenues. Finally, the average ratio of total debt service to GNI is 4.48%, while the median is 3.64%. The range of 0.826% to 11.97% and the standard deviation of 3.80% indicate the variability of Zambia’s debt service obligations. High debt service obligations can strain public finances and limit the government’s ability to spend in critical areas, even if debt service has historically been sufficient. To address these issues, Zambia needs to establish long-term debt service plans that balance fiscal restraint with economic expansion.

Correlation Analysis

Several notable correlations among Zambia’s key macroeconomic variables are shown in the correlation matrix in Table 2. These relationships show how inflation, economic growth, debt levels, and investment interact and point to important areas for government action.

Table 2: Correlation Matrix of Key Macroeconomic Indicators

|

Inflation, consumer prices (annual %) |

GDP growth (annual %) |

Foreign direct investment, net inflows (% of GDP) |

Gross fixed capital formation (% of GDP) |

Total debt service (% of GNI) |

External debt stocks (% of GNI) |

||

|---|---|---|---|---|---|---|---|

|

Inflation, consumer prices (annual %) |

Pearson's r |

— |

|

|

|

|

|

|

|

df |

— |

|

|

|

|

|

|

|

p-value |

— |

|

|

|

|

|

|

GDP growth (annual %) |

Pearson's r |

-0.235 |

— |

|

|

|

|

|

|

df |

12 |

— |

|

|

|

|

|

|

p-value |

0.418 |

— |

|

|

|

|

|

Foreign direct investment, net inflows (% of GDP) |

Pearson's r |

-0.454 |

0.432 |

— |

|

|

|

|

|

df |

12 |

12 |

— |

|

|

|

|

|

p-value |

0.103 |

0.123 |

— |

|

|

|

|

Gross fixed capital formation (% of GDP) |

Pearson's r |

0.052 |

-0.498 |

-0.039 |

— |

|

|

|

|

df |

12 |

12 |

12 |

— |

|

|

|

|

p-value |

0.859 |

0.070 |

0.895 |

— |

|

|

|

Total debt service (% of GNI) |

Pearson's r |

0.542* |

-0.692** |

-0.655* |

0.258 |

— |

|

|

|

df |

12 |

12 |

12 |

12 |

— |

|

|

|

p-value |

0.045 |

0.006 |

0.011 |

0.373 |

— |

|

|

External debt stocks (% of GNI) |

Pearson's r |

0.519 |

-0.705** |

-0.539* |

0.409 |

0.888*** |

— |

|

|

df |

12 |

12 |

12 |

12 |

12 |

— |

|

|

p-value |

0.057 |

0.005 |

0.047 |

0.147 |

< .001 |

— |

|

Note. * p < .05, ** p < .01, *** p < .001 |

|||||||

Inflation and GDP growth are negatively correlated with a value of -0.235. The lack of statistical significance in this relationship (p = 0.418) shows that slower economic growth in Zambia is not always associated with higher inflation. Although inflation is often predicted to be detrimental to development by reducing the purchasing power of consumers and increasing the cost of doing business, the minimal association in this case calls for a more complete examination of the underlying structural issues affecting the Zambian economy. Higher inflation is associated with a higher debt service burden, as evidenced by the significant positive association between inflation and total debt service (0.542, p = 0.045). This relationship may be affected by the impact of inflation on interest rates and exchange rate depreciation, which increases the cost of servicing external debt. This result underscores the importance of inflation control in maintaining Zambia’s debt sustainability and fiscal stability. The external debt stock and GDP growth have a significant negative correlation (-0.705, p = 0.005), suggesting that slower economic development is associated with higher levels of external debt. The crowding out effect, which occurs when large debt obligations limit the resources available for beneficial investments in infrastructure, education, and other critical sectors, can be used to explain this relationship. The study highlights the need for policies that balance debt accumulation with long-term economic growth and the potential risks of over-reliance on external borrowing. FDI and external debt have a negative relationship (-0.539, p = 0.047), suggesting that high debt levels may discourage foreign investment. This may be due to investors’ concerns about Zambia’s macroeconomic stability, fiscal sustainability, and the government’s ability to implement investor-friendly policies. If Zambia’s high debt levels prevent the government from offering incentives or improving infrastructure, the country may become less attractive to foreign investors. There is a significant positive correlation between external debt stock and total debt service (0.888, p < 0.001). This shows that higher debt burdens could be associated with higher debt service obligations. This relationship underscores the need for effective debt management strategies to prevent rising debt service costs from diverting resources from essential government spending and economic growth initiatives. The marginally significant inverse relationship between GDP growth and gross fixed capital formation (-0.498, p = 0.070) is an interesting finding in Table 2. This implies that higher fixed investment does not lead to rapid economic growth, either because of inefficient investment allocation, delays in project completion, or the prevalence of capital-intensive projects with long gestation periods. To maximize the contribution of investment to economic growth, policymakers should consider ways to improve investment efficiency.

The correlation matrix illustrates Zambia’s economic situation, which is characterized by low inflation, uneven GDP growth, and significant dependence on external debt. In addition to highlighting the need for effective debt management strategies, the study raises important questions about the negative impact of high debt levels on foreign investment and economic expansion. Moreover, sustaining long-term growth will depend on ensuring that investments generate measurable financial returns. Structural reforms, effective macroeconomic policies, and fiscal restraint would be needed to improve Zambia’s economic stability and resilience.

The presented correlation matrix provides valuable insights into the relationships between Zambia’s key macroeconomic indicators during the study period. These interrelationships reveal the ways in which inflation dynamics, foreign investment, debt accumulation and capital formation affect overall economic performance, offering valuable policy insights.

Stationarity Analysis of Zambia’s Macroeconomic Variables

Stationarity tests are crucial for time series analysis, as they ensure that the statistical properties of a variable, such as the mean and variance, do not change over time. Non-stationary series can produce misleading regression results.

Table 3: ADF Test Results on Levels

|

Variable |

Dickey-Fuller Statistic |

p-value |

Stationary |

|---|---|---|---|

|

GDP growth (annual %) |

-1.2544 |

0.8564 |

No (Non-stationary) |

|

Inflation, consumer prices (annual %) |

-3.8855 |

0.0296 |

Yes (Stationary) |

|

External debt stocks (% of GNI) |

-0.7707 |

0.9524 |

No (Non-stationary) |

|

Foreign direct investment, net inflows (% of GDP) |

-3.1195 |

0.1459 |

No (Non-stationary) |

Table 3 shows that inflation has remained stable, indicating consistent statistical properties over time. However, GDP growth, external debt and foreign direct investment (FDI) are non-stationary, suggesting the presence of potential trends or other non-constant behaviours.

Table 4: ADF Test Results on First Differences

|

Variable Difference |

Dickey-Fuller Statistic |

p-value |

Stationary? |

|---|---|---|---|

|

Difference of GDP growth |

-2.7344 |

0.2926 |

No (Still Non-stationary) |

|

Difference of Inflation |

-2.8204 |

0.2598 |

No (Still Non-stationary) |

|

Difference of External debt |

1.0601 |

0.9900 |

No (Still Non-stationary) |

|

Difference of FDI |

-1.5869 |

0.7297 |

No (Still Non-stationary) |

First differencing was applied to remove trends, as non-stationarity was detected in most of the variables. However, as shown in Table 4, first differencing did not make these variables stationary, as indicated by the high p-values. This suggests the need for further transformation, such as second differencing, or consideration of alternative approaches to stationarity, such as detrending or seasonal adjustments. Alternatively, the limited sample size or data frequency may have affected the statistical power of the test.

Table 5 shows the analysis of the two different measures of debt service in relation to external debt stocks. Both debt service indicators exhibit strong, statistically significant positive correlations with external debt. Therefore, including both measures in further regression models is justified, as they provide complementary perspectives on Zambia’s debt sustainability.

Table 5: Correlation Between Debt Measures

|

Pair of Variables |

Correlation Coefficient (r) |

p-value |

Interpretation |

|---|---|---|---|

|

External debt stocks (% of GNI) & Total debt service (% of GNI) |

0.888 |

< 0.0001 |

Strong positive correlation |

|

External debt stocks (% of GNI) & Total debt service (% of exports of goods, services and primary income) |

0.837 |

0.0002 |

Strong positive correlation |

Table 5 presents an analysis of two measures of debt servicing relative to external debt. Both debt service indicators demonstrate a strong, statistically significant positive correlation with external debt. These results support the usefulness of these indicators in assessing different dimensions of sustainability. However, potential multicollinearity issues should be assessed before including the variables simultaneously in future econometric models.

Regression Analysis

Three regression models were estimated to explore the determinants of GDP growth and debt service burdens.

Model 1: Determinants of GDP Growth

This regression model in Table 6 evaluates the influence of gross fixed capital formation, external debt, and inflation on GDP growth. The model is specified as:

GDP Growth = β₀ + β₁(Gross Fixed Capital Formation) + β₂(External Debt) + β₃(Inflation) + ϵ

Table 6: Determinants of GDP Growth

|

Variable |

Estimate |

Std. Error |

t-value |

p-value |

|---|---|---|---|---|

|

Intercept |

10.4217 |

4.1814 |

2.492 |

0.0319 * |

|

Gross fixed capital form. |

-0.1290 |

0.1329 |

-0.971 |

0.3546 |

|

External debt stocks |

-0.0405 |

0.0163 |

-2.483 |

0.0324 * |

|

Inflation |

0.0809 |

0.1561 |

0.518 |

0.6156 |

Intercept (10.42): The model predicts a baseline GDP growth rate of 10.42% when all explanatory variables are set to zero. While this is statistically significant (p = 0.0319), it is difficult to interpret practically because zero values for the predictors are unrealistic.

External Debt Stocks: The external debt coefficient is -0.0405, which is statistically significant (p = 0.0324). This indicates that, holding other factors constant, GDP growth decreases by approximately 0.04 percentage points for every unit increase in external debt (as measured in the model). This suggests that higher debt levels may have a crowding-out effect on economic performance by reducing available resources for productive investments.

Gross Fixed Capital Formation: Although it is theoretically expected to drive growth, the coefficient is -0.1290, which is not statistically significant (p = 0.3546). The negative sign is counterintuitive and may reflect measurement lags, inefficiencies in capital allocation, or other contextual factors, such as poor project execution.

Inflation: The inflation coefficient is 0.0809, but it is not statistically significant (p = 0.6156). This implies that, based on the available data, inflation does not clearly or consistently affect GDP growth. Depending on the inflation level and economic context (e.g., moderate vs. high inflation), the direction and magnitude of its impact may vary.

With an Adjusted R² of 0.4308, the model explains approximately 43.1% of the variation in GDP growth. This indicates a moderate level of explanatory power and suggests that, while the model captures some key drivers of growth, it may not include other important factors.

In a nutshell external debt is a statistically significant negative determinant of GDP growth, highlighting the economic risks of high debt levels. Conversely, gross fixed capital formation and inflation do not have statistically significant effects in this model.

Model 2: Debt Service (% of GNI)

As shown in Table 7, the regression model examines the relationship between external debt and foreign direct investment (FDI), as well as the debt service burden, which is measured as a percentage of gross national income (GNI). The model is specified as follows:

Debt Service (% of GNI) = β₀ + β₁(External Debt Stocks) + β₂(FDI) + ϵ

Table 7. Debt Service (% of GNI)

|

Variable |

Estimate |

Std. Error |

t-value |

p-value |

|---|---|---|---|---|

|

External debt stocks |

0.05875 |

0.01482 |

3.965 |

0.00328 ** |

|

FDI |

-0.28976 |

0.22069 |

-1.313 |

0.22169 |

E

xternal Debt Stocks: The coefficient is 0.05875, which is statistically significant at the 1% level (p = 0.00328). This indicates a strong positive relationship between external debt and the debt-service-to-GNI ratio. Specifically, a one-unit increase in external debt is associated with a 0.06 percentage point increase in the debt service burden, holding all other factors constant. Therefore, as Zambia accumulates debt, its repayment obligations increase significantly, which could strain fiscal resources and divert funds from development priorities.

Foreign Direct Investment (FDI): The FDI coefficient is -0.28976, indicating a negative association with debt service. However, this result is not statistically significant (p = 0.22169), suggesting that FDI does not reliably or consistently impact debt service burdens within the scope of this model. The negative sign implies the theoretical expectation that increased FDI inflows could reduce reliance on debt financing; however, this relationship is not supported by the data in this instance.

An Adjusted R² value of 0.7651 indicates that the model explains about 76.5% of the variation in debt service as a percentage of GNI. This indicates strong explanatory power, with external debt stocks emerging as the dominant predictor.

The results highlight that external debt is a significant driver of the debt service burden, emphasizing the fiscal pressures that accompany rising debt levels. Although foreign direct investment (FDI) is negatively associated with debt service, its effect is not statistically robust in this model. These findings reinforce the importance of prudent external borrowing and the potential role of FDI as a complementary financing source that could reduce debt dependence if scaled effectively.

Model 3: Debt Service (% of Exports)

As shown in Table 8, the regression model explores the impact of a country’s external debt on its debt service obligations, expressed as a percentage of export earnings. The model is specified as follows:

Debt Service (% of Exports) = β₀ + β₁(External Debt Stocks) + ϵ

Table 8. Debt Service (% of Exports)

|

Variable |

Estimate |

Std. Error |

t-value |

p-value |

|---|---|---|---|---|

|

External debt stocks |

0.1292 |

0.0431 |

2.996 |

0.015 * |

External Debt Stocks: The estimated coefficient of 0.1292 is statistically significant at the 5% level (p = 0.015). This indicates a strong, positive relationship between external debt and debt service as a percentage of exports. For every one-unit increase in external debt, the debt service burden relative to exports rises by approximately 0.13 percentage points. This finding underscores the vulnerability of export earnings to rising external debt obligations and highlights a critical dimension of debt sustainability in economies that depend on exports.

An Adjusted R² value of 0.6416 indicates that approximately 64.2% of the variation in the debt-to-export ratio is explained by changes in external debt. This is a solid level of explanatory power for a single-variable model and affirms that external debt is a key predictor of export-based debt servicing pressures.

Model limitations

Although the regression analyses presented are methodologically sound and the interpretations align with statistical and theoretical expectations, there are several limitations that require explicit acknowledgement, which uses a univariate specification. These limitations do not compromise the validity of the empirical results but rather delineate the boundaries within which the findings should be interpreted.

Implications for future research

To enrich the analytical depth and enhance causal inference, future research should expand the model to incorporate additional macroeconomic, financial and structural variables. The use of multivariate or panel regression techniques, which can better account for heterogeneity and endogeneity, would also strengthen the robustness of subsequent analyses. Such extensions would provide a more holistic understanding of the determinants of debt servicing outcomes in different economic contexts.

Summary

Regression analysis provides critical insights into Zambia’s external debt dynamics and their broader macroeconomic implications. A strong, statistically significant relationship exists between external debt and debt service ratios, both expressed as percentages of GNI and exports. This highlights the persistent challenge Zambia faces in ensuring external debt sustainability. Rising debt levels clearly translate into higher repayment burdens, straining national resources. Furthermore, the negative impact of external debt on GDP growth suggests that excessive borrowing may constrain economic expansion by crowding out private investment or increasing macroeconomic uncertainty. Interestingly, inflation does not emerge as a significant predictor of GDP growth or debt service, suggesting that other macroeconomic variables may play a more decisive role in shaping Zambia’s economic trajectory. The absence of a statistically significant relationship between gross fixed capital formation and GDP growth may indicate delays in economic returns on investment, inefficiencies in capital utilization, or data limitations. Overall, these findings underscore the importance of prudent debt management, improved investment efficiency, and broader structural reforms to enhance Zambia’s economic resilience.

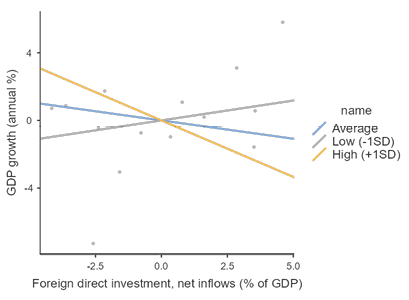

Moderation Analysis of FDI and External Debt on GDP Growth in Zambia

The moderation analysis examines how Zambia’s GDP growth (annual percentage) is affected by the relationship between net foreign direct investment (FDI) inflows (as a percentage of GDP) and the external debt stock (as a percentage of GNI). The results are analyzed in the light of Zambia’s economic situation and presented in two tables.

The external debt stock and FDI have a significant interaction effect on GDP growth, as shown in Table 9. The coefficient of the interaction term (FDI * external debt stock) is -0.00936 (p = 0.042), indicating that the level of external debt affects the relationship between FDI and GDP growth. This result suggests that the relationship between FDI and economic growth in Zambia is influenced by external debt.

On average, FDI inflows do not have a significant direct impact on GDP growth as evidenced by the negative but statistically insignificant independent effect of net FDI inflows on GDP growth (-0.21653, p = 0.260).

On the other hand, GDP growth is significantly hampered by the stock of external debt (-0.05784, p < 0.001), supporting previous findings that high levels of external debt are associated with poorer economic performance. This is likely due to the crowding out effect that occurs when debt service obligations divert resources available for profitable investments. The significant interaction term shows that the impact of foreign direct investment (FDI) on GDP growth declines as external debt increases. This is probably because investors perceive greater risk and the government is less able to support investment-led growth.

Table 9: Moderation Estimates

|

Estimate |

SE |

Z |

p |

|

|---|---|---|---|---|

|

Foreign direct investment, net inflows (% of GDP) |

-0.21653 |

0.19218 |

-1.13 |

0.260 |

|

External debt stocks (% of GNI) |

-0.05784 |

0.01052 |

-5.50 |

< .001 |

|

Foreign direct investment, net inflows (% of GDP) * External debt stocks (% of GNI) |

-0.00936 |

0.00461 |

-2.03 |

0.042 |

The interaction effect between FDI and GDP growth at different levels of external debt is examined in the following simple slope analysis, as shown in Table 10. The results show that the effect of FDI on GDP growth depends on whether the external debt is low, average or high.

FDI has a negative but statistically insignificant effect on GDP growth at the average level of external debt (-0.217, p = 0.340). This implies that FDI inflows have little impact on Zambia’s economic growth under typical debt conditions. The lack of relevance suggests that external debt alone does not significantly alter the relationship between FDI and economic performance.

FDI has a positive but statistically insignificant effect on GDP growth when external debt is low (0.235, p = 0.410). This implies that FDI inflows may slightly boost economic growth in a low debt environment, but not enough to be considered significant. This may suggest that even in the presence of favorable financial conditions, the Zambian economy has structural impediments that prevent the full realization of FDI.

However, at high levels of external debt, FDI has a negative and marginally significant impact on GDP growth (-0.668, p = 0.069). This suggests that higher levels of external debt are associated with slower economic growth compared to FDI inflows. The negative effect is likely due to the adverse macroeconomic environment created by a high debt burden, which reduces fiscal capacity, discourages productive investment, and increases economic uncertainty. Consequently, FDI may not boost growth in a highly indebted country, underscoring the importance of debt sustainability in optimizing the benefits of foreign investment.

Table 10: Simple Slope Estimates

|

Estimate |

SE |

Z |

p |

|

|---|---|---|---|---|

|

Average |

-0.217 |

0.227 |

-0.954 |

0.340 |

|

Low (-1SD) |

0.235 |

0.285 |

0.823 |

0.410 |

|

High (+1SD) |

-0.668 |

0.367 |

-1.819 |

0.069 |

|

Note. shows the effect of the predictor (Foreign direct investment, net inflows (% of GDP)) on the dependent variable (GDP growth (annual %)) at different levels of the moderator (External debt stocks (% of GNI)) |

||||

The results of the moderation analysis shed important light on the complex relationship between FDI, external debt, and economic growth in Zambia. The results show that regardless of the level of external debt, FDI alone does not significantly increase GDP growth. This could be due to inefficient use of FDI, the hegemony of the mining industry in attracting foreign capital, or a lack of linkages between FDI and the economy as a whole.

In addition, the potential benefits of FDI appear to be diminished by high levels of external debt. An adverse economic climate created by rising debt levels can discourage future investment, increase macroeconomic volatility, and reduce the ability of FDI to stimulate growth. As a result, excessive reliance on external borrowing could have unforeseen consequences that hinder rather than promote economic expansion. Although lower levels of external debt create a more conducive business environment, the benefits of foreign direct investment (FDI) are statistically insignificant. This underscores the need for significant structural changes, including improving the business climate, strengthening governance, and investing in infrastructure, to reap the full development benefits of FDI.

These findings underscore the importance for Zambia to manage its debt responsibly. Reducing the external debt burden and creating an investment-friendly environment are essential if FDI is to make a substantial contribution to sustainable economic growth. To reduce the negative effects of excessive debt and increase the contribution of FDI to Zambia’s sustainable economic growth, it is necessary to strengthen institutions, maintain policy consistency, and promote economic diversification.

Discussion

This study provides a thorough analysis of Zambia’s macroeconomic performance, with a focus on inflation, gross domestic product (GDP) growth, foreign direct investment (FDI), gross fixed capital formation, external debt, and debt servicing obligations. Through the use of descriptive statistics, correlation analysis, stationarity tests, regression analysis, and moderation models, the study provides a nuanced understanding of the macroeconomic dynamics that shape Zambia’s economic resilience.

Descriptive statistics reveal an environment of persistently high and volatile inflation, with an average rate of 10.51% and a standard deviation of 4.78%. Inflation ranged from 6.43% to 22.02%, with a median of 8.83%. These fluctuations align with the findings of Silvia et al. (2023) and Jackson (2024), who highlight the impact of supply-side constraints and exchange rate instability on inflation in developing countries. Furthermore, the findings corroborate those of Sani et al. (2024), who emphasize that inflation above 10% significantly hinders GDP growth. This study corroborates the idea that persistent inflation undermines real incomes and necessitates more effective monetary policy responses.

With an average GDP growth of 4.49% and a standard deviation of 2.98%, Zambia’s economy exhibits moderate yet volatile expansion, ranging from -2.79% to 10.30%. This is consistent with Nel et al. (2017), who attribute Zambia’s economic volatility to its reliance on copper exports and global commodity price cycles. The observed instability underscores the need for structural reforms to foster diversification and long-term resilience.

Foreign direct investment (FDI) inflows averaged 3.94% of GDP but showed significant variability ranging from -0.22% to 8.53%. The negative correlation between FDI and external debt (r = -0.539, p = 0.047) aligns with the arguments of Ndaba (2015) and Ndlovu and Haabazoka (2024) that excessive debt erodes investor confidence. This study reinforces the idea that debt sustainability is necessary for attracting and retaining FDI, as Yangailo (2024b) has suggested.

With an average of 30.64% of GDP, gross fixed capital formation signals strong investment levels. However, its negative correlation with GDP growth (r = -0.498, p = 0.070) raises concerns about investment efficiency. These finding echoes those of Ndaba (2015) and Claudio-Quiroga et al. (2022). Despite high capital spending, misallocation and governance inefficiencies may limit its impact on growth. This reaffirms the importance of quality over quantity in public investment.

External debt averaged 69.77% of GNI, reaching a maximum of 168.40%, which indicates severe debt stress. The strong positive correlation between debt and debt service (r = 0.888, p < 0.001) and the significant negative correlation between debt and GDP growth (r = −0.705, p = 0.005) validate the debt overhang hypothesis described by Mammadli et al. (2021). This study confirms that high debt servicing crowds out productive investment, a view supported by Hilton (2021) and Manasseh et al. (2022).

A significant positive correlation (r = 0.542, p = 0.045) between inflation and debt service suggests that inflation exacerbates repayment burdens, possibly through currency depreciation and rising nominal interest rates. This mechanism was also discussed by Oyadeyi et al. (2024).

Stationarity tests reveal that inflation is stationary, but that GDP growth, external debt, and foreign direct investment (FDI) are non-stationary, even after differencing. These findings suggest structural breaks and long-term trends that are consistent with Zambia’s cyclical macroeconomic vulnerabilities, as described by El Aboudi and Khanchaoui (2021).

The regression results support the debt-growth nexus. Model 1 shows that external debt negatively impacts growth (coefficient = -0.0405, p = 0.032), thus validating the crowding-out hypothesis. Investment and inflation were insignificant, highlighting short-run inefficiencies and policy constraints. Model 2 shows that external debt significantly increases debt servicing as a percentage of GNI (coefficient = 0.05875, p = 0.003). Foreign direct investment (FDI) has no mitigating effect, a result consistent with Nistor (2014). Additionally, the results show that external debt raises debt servicing relative to exports (coefficient = 0.1292, p = 0.015), indicating vulnerability to trade shocks.

Moderation analysis reveals that FDI positively affects growth at low debt levels (coefficient = 0.235, p = 0.410) but negatively affects growth at high debt levels (coefficient = -0.668, p = 0.069). The significant interaction term (-0.00936, p = 0.042) confirms that debt diminishes the growth-promoting potential of FDI, as Zekarias (2016) and Yangailo (2024b) have argued. These findings align with the view that weak institutional quality and high debt levels limit the benefits of foreign investment.

Overall, these findings reinforce prior research by Harmon (2012), Osewe (2017), and Sundus et al. (2022). They emphasize that Zambia’s macroeconomic challenges, especially debt, inflation, and inefficient investment, are mutually reinforcing and impede sustainable growth.

Practical and Theoretical Implications

Theoretical Implications

Debt Overhang Hypothesis Validated: The study reinforces the debt overhang hypothesis, which states that high external debt discourages domestic and foreign investment, thereby reducing growth. The strong negative correlation between debt and GDP growth, coupled with increased debt servicing costs, empirically validates the theoretical work of previous studies.

Crowding-Out Effect of Public Debt: The regression results support the theory that excessive debt servicing displaces public investment in growth-promoting sectors. These results contribute to the literature on fiscal constraints in developing economies.

FDI-Debt Interaction Theory Confirmed: The moderation model confirms that the effectiveness of foreign direct investment (FDI) in stimulating growth diminishes in high-debt environments. This finding aligns with Zekarias (2016) and adds nuance to the theory. The efficacy of FDI depends on macroeconomic fundamentals, such as debt sustainability and institutional capacity.

Public Investment Efficiency Debate: The negative correlation between gross fixed capital formation and GDP growth challenges traditional growth theories which assume a positive, direct relationship between capital formation and output. This finding aligns with recent critiques that emphasize the importance of investment quality, governance, and absorptive capacity (Claudio-Quiroga et al., 2022).

Inflation-Growth Nonlinearity: The negative association between inflation and growth supports nonlinear models in which inflation below certain thresholds may be benign or growth-neutral but becomes harmful above them (e.g., above 10%). This finding aligns with the work of Sani et al. (2024) and other threshold inflation-growth models.

Practical Implications

Debt Management is Central to Growth: The strong negative impact of external debt on GDP growth and debt servicing costs underscores the urgent need for Zambia to implement prudent borrowing strategies and restructure unsustainable debt, thereby averting macroeconomic instability.

FDI Policy Must Be Paired with Debt Reform: The diminishing returns of FDI under high debt stress suggest that investment promotion alone is insufficient. Zambia must address debt sustainability and institutional weaknesses to fully benefit from FDI inflows.

Public Investment Reform Required: Despite high levels of gross fixed capital formation, the absence of growth dividends suggests inefficiencies likely resulting from poor project selection, corruption, or limited capacity. Therefore, strengthening public investment management systems (PIMS) is critical.

Inflation Control as a Foundation for Stability: High and volatile inflation persistently undermines economic planning, real incomes, and investment confidence. Sustainable inflation stabilization requires robust coordination between monetary and fiscal policies.

Export Dependency and Trade Vulnerability: The vulnerability of debt service to export fluctuations indicates a narrow export base. Therefore, trade diversification is imperative to cushion against external shocks and stabilize debt sustainability ratios.

Recommendations

In the short term, Zambia should engage with multilateral creditors and international partners to restructure and extend repayment timelines, implementing a comprehensive debt sustainability strategy. In the medium term, Zambia must strengthen debt transparency and accountability through legislative reforms and regular public debt audits. In the long term, Zambia should establish binding fiscal rules directly linked to productive investment returns to ensure that debt is only incurred for projects that yield measurable economic benefits.

It is also critical to enhance the efficiency of public investment. This can be achieved by conducting rigorous cost-benefit analyses of major projects before allocating funds, thereby ensuring that public resources are allocated to high-impact areas. An independent Public Investment Appraisal Authority can evaluate and approve major capital projects based on objective criteria. Furthermore, project disbursements should be tied to results and outputs rather than inputs or political cycles to promote accountability and performance-oriented budgeting.

To stabilize and reduce inflation, the independence of the central bank must be strengthened, and its capacity to manage inflation through forward-looking monetary policy tools must be enhanced. Coordinating with fiscal authorities is necessary to prevent pro-cyclical spending and curb off-budget expenditures that fuel inflation. Additionally, supporting local food production and reducing dependence on imports can address supply-side inflationary pressures and enhance price stability.

Foreign direct investment (FDI) policy should align with broader institutional and fiscal reforms. The focus should shift toward attracting FDI that seeks efficiency and technology transfer, rather than purely resource-seeking investors. Providing regulatory certainty and consistent tax policies will boost investor confidence. Creating Special Economic Zones (SEZs) with embedded governance, monitoring, and arbitration mechanisms will further reassure investors and foster a more favorable business environment.

Another key recommendation is diversifying the export base. Zambia should promote adding value to its copper and other raw materials by supporting downstream industries, such as battery manufacturing and wiring production. Strategic sectors, including agro-processing, tourism, and ICT-enabled services, should be developed to reduce reliance on traditional exports. Additionally, the country should negotiate trade agreements that expand market access beyond traditional trading partners to tap into new opportunities.

Institutional capacity building is essential for achieving macroeconomic stability. Improving fiscal management requires strengthening institutions such as the Zambia Revenue Authority (ZRA), the Ministry of Finance, and the Bank of Zambia by providing them with modern digital tools, targeted training, and enhanced audit capabilities. Investing in public sector reforms that enhance procurement systems, financial oversight, and anti-corruption enforcement will build public trust and improve governance.

Finally, data, research, and monitoring should be institutionalized. Creating a Macroeconomic Policy Research Unit within the Ministry of Finance will allow the government to model, monitor, and evaluate the implications of its policy decisions in real time. These efforts should be complemented by strong partnerships with universities and think tanks to generate evidence-based, homegrown policy innovations tailored to Zambia’s unique development context.

Conclusion

This study offers a thorough examination of Zambia’s macroeconomic performance, revealing the interconnected challenges that persistently hinder sustainable growth and economic resilience. The findings reveal that persistent inflation, high external debt, volatile GDP growth, and inefficiencies in public investment are deeply intertwined, creating a cyclical pattern of macroeconomic vulnerability. Statistical evidence underscores the critical roles of debt sustainability, efficient capital formation, and a conducive investment climate in shaping Zambia’s long-term development trajectory. Notably, the negative correlation between external debt and GDP growth confirms the debt overhang hypothesis. Additionally, the moderation analysis illustrates that high debt levels diminish the growth-enhancing potential of foreign direct investment. These results reinforce the idea that macroeconomic instability is a cause and consequence of weak institutions, poor investment planning, and inadequate policy coordination.

Theoretical implications highlight the importance of incorporating fiscal discipline, institutional quality, and economic diversification into development strategies. The empirical results support established economic theories, such as the crowding-out effect of debt, the inefficiency hypothesis of public investment, and the conditionality of foreign direct investment (FDI) impact based on host country governance and macroeconomic stability. In practice, the study emphasizes the urgent need for policy actions to stabilize inflation, reduce debt burdens, and improve the allocation and productivity of public resources. Essential steps for building a resilient and inclusive economy include reforming the investment framework to attract high-quality foreign direct investment (FDI), enhancing institutional capacity, and leveraging data-driven policy design.

Ultimately, Zambia’s path to sustained economic growth requires an evidence-based, transparent, and reform-oriented macroeconomic strategy. The recommendations provided, ranging from debt management and inflation control to export diversification and public investment reform, serve as a roadmap for policymakers to address systemic challenges. If implemented effectively, these interventions can break the cycle of vulnerability and unlock the country’s potential for equitable and sustainable development.

References

Arnone, M., Bandiera, L., & Presbitero, A. (2008). Debt sustainability framework in HIPCs: A critical assessment and suggested improvements. Available at SSRN 871171.

Bank of Zambia. (2025). Statistics. https://www.boz.zm/statistics.htm

Claudio-Quiroga, G., Gil-Alana, L. A., & Maiza-Larrarte, A. (2022). The impact of China’s FDI on economic growth: Evidence from Africa with a long memory approach. Emerging Markets Finance and Trade, 58(6), 1753-1770.

EL Aboudi, S., & Khanchaoui, I. (2021). Exploring the impact of inflation and external debt on economic growth in Morocco: An empirical investigation with an ARDL approach. Asian Economic and Financial Review, 11(11), 894. DOI:10.18488/journal.aefr.2021.1111.894.907

El-Mahdy, A. M., & Torayeh, N. M. (2009). Debt sustainability and economic growth in Egypt. International journal of Applied Econometrics and quantitative studies, 6(1), 21-55.

Girdzijauskas, S., Streimikiene, D., Griesiene, I., Mikalauskiene, A., & Kyriakopoulos, G. L. (2022). New approach to inflation phenomena to ensure sustainable economic growth. Sustainability, 14(1), 518. https://doi.org/10.3390/su14010518

Harmon, E. Y. (2012). The impact of public debt on inflation, GDP growth and interest rates in Kenya. Dissertation, University of Nairobi.

Hilton, S. K. (2021). Public debt and economic growth: contemporary evidence from a developing economy. Asian Journal of Economics and Banking, 5(2), 173-193. https://doi.org/10.1108/AJEB-11-2020-0096

Iqbal, M., Arif, A. S., Jadoon, A. K., & Rana, A. D. (2023). The impact of debt service and inflation on economic growth in Pakistan: Evidence from ARDL model and approximate Bayesian analysis. Pakistan Journal of Commerce and Social Sciences (PJCSS), 17(2), 263-287. https://hdl.handle.net/10419/278052

Jackson, E. A. (2024). Economic Theory of Inflation. ZBW - Leibniz Information Centre for Economics, Kiel, Hamburg. https://hdl.handle.net/10419/280999

Liu, Y., Savastano, M., & Zettelmeyer, J. (2020). The International Architecture for Resolving Sovereign Debt Involving Private-Sector Creditors: Recent Developments, Challenges, and Reform Options. Washington: International Monetary Fund.

Mammadli, M., Sadik-Zada, E., Gatto, A., & Huseynova, R. (2021). What drives public debt growth?: A focus on natural resources, sustainability and development. International Journal of Energy Economics and Policy, 11(5), 614-621.

Manasseh, C. O., Abada, F. C., Okiche, E. L., Okanya, O., Nwakoby, I. C., Offu, P., ... & Nwonye, N. G. (2022). External debt and economic growth in Sub-Saharan Africa: Does governance matter?. Plos one, 17(3), e0264082. https://doi.org/10.1371/journal.pone.0264082

Muhammad, A. A. (2023). Examining the relationship among unemployment, inflation, and economic growth. Journal of Business and Economic Options, 6(2), 23-31.

Ndaba, S. (2015). The Impact of Foreign Direct Investment on Economic Growth in Zambia: A study in the context of a natural resource dependent economy. International Institute of Social Studies.

Ndlovu, D., & Haabazoka, L. (2024). Evaluating the Impact of Foreign Direct Investment on Economic Growth in Zambia; 1996-2020. East African Finance Journal, 3(1), 107-130.

Nel, E., Smart, J., & Binns, T. (2017). Resilience to economic shocks: reflections from Zambia’s Copperbelt. Growth and Change, 48(2), 201-213. https://doi.org/10.1111/grow.12181

Nistor, P. (2014). FDI and economic growth, the case of Romania. Procedia Economics and Finance, 15, 577-582.

Osewe, V. O. (2017). Effect of external debt and inflation on economic growth in Kenya (Dissertation). KCA University. URI: http://41.89.49.13:8080/xmlui/handle/123456789/732

Oyadeyi, O. O., Agboola, O. W., Okunade, S. O., & Osinubi, T. T. (2024). The debt-growth nexus and debt sustainability in Nigeria: Are there reasons to be concerned?. Journal of Policy Modeling, 46(1), 129-152. https://doi.org/10.1016/j.jpolmod.2023.11.004

Panizza, U., Sturzenegger, F., & Zettelmeyer, J. (2009). The economics and law of sovereign debt and default. Journal of economic literature, 47(3), 651-698.

Pegkas, P. (2015). The impact of FDI on economic growth in Eurozone countries. The Journal of Economic Asymmetries, 12(2), 124-132.

Reinhart, C. M., & Rogoff, K. S. (2009). This time is different: Eight centuries of financial folly. princeton university press.

Sani, A. S., Lukman, H., Tetuko, R. P., & Putra, P. (2024). The Impact of Inflation on the Business Cycle and Economic Growth: An Empirical Analysis. InternationalJournalonEconomics, FinanceandSustainableDevelopment (IJEFSD), 6(11), 274-286.

Sharaf, M. F., & Shahen, A. M. (2023). Does external debt drive inflation in Sudan: evidence from symmetric and asymmetric ARDL approaches. Journal of Business and Socio-Economic Development, 3(4), 293-307. https://doi.org/10.1108/JBSED-03-2023-0023

Silvia, E., Sihotang, N. V., & Sihotang, D. (2023). Causality Analysis of Inflation and Economic Growth Using the Error Correction Model (ECM). Indonesia Accounting Research Journal, 11(1), 23-36.

Sundus, Naveed, S., & Islam, T. U. (2022). An empirical investigation of determinants & sustainability of public debt in Pakistan. Plos one, 17(9), e0275266. https://doi.org/10.1371/journal.pone.0275266

World Bank. ( 2025).World Bank Open Data. https://data.worldbank.org/

Yangailo, T. (2024a). Public debt–economic growth nexus: A systematic literature review. Journal of Developing Economies (JDE), 9(2), Article 54959. https://doi.org/10.20473/jde.v9i2.54959

Yangailo, T. (2024b). El impacto de la inversión extranjera directa en el crecimiento económico de Zambia: Un análisis exhaustivo. Revista Científica Profundidad Construyendo Futuro, 21(21), 50–57. https://doi.org/10.22463/24221783.4637

Zekarias, S. M. (2016). The impact of foreign direct investment (FDI) on economic growth in Eastern Africa: Evidence from panel data analysis. Applied Economics and Finance, 3(1), 145-160.

Appendices

Macroeconomic Indicators for Zambia (2010-2023)

|

Year |

Inflation, consumer prices (annual %) |

GDP growth (annual %) |

Foreign direct investment, net inflows (% of GDP) |

Agriculture, forestry, and fishing, value added (% of GDP) |

Gross fixed capital formation (% of GDP) |

Total debt service (% of GNI) |

Total debt service (% of exports of goods, services and primary income) |

External debt stocks (% of GNI) |

|---|---|---|---|---|---|---|---|---|

|

2010 |

8.501761 |

10.29822 |

8.533196 |

9.420946 |

25.89122 |

0.825771 |

1.935973 |

22.88037 |

|

2011 |

6.429397 |

5.569252 |

4.725162 |

9.648058 |

27.9747 |

1.014473 |

2.399254 |

23.33314 |

|

2012 |

6.5759 |

7.597381 |

6.789381 |

9.32164 |

23.87785 |

0.962739 |

2.294169 |

24.70641 |

|

2013 |

6.977676 |

5.057537 |

7.489325 |

8.226523 |

25.8004 |

1.316736 |

3.050385 |

24.87638 |

|

2014 |

7.806876 |

4.693283 |

5.555428 |

6.779598 |

31.03771 |

1.64325 |

3.944447 |

36.39053 |

|

2015 |

10.11059 |

2.920375 |

7.447417 |

4.980837 |

38.45314 |

2.776743 |

7.029519 |

59.21249 |

|

2016 |

17.86973 |

3.7551 |

3.16252 |

6.228472 |

36.42059 |

3.861228 |

10.47072 |

77.7495 |

|

2017 |

6.577312 |

3.525863 |

4.280501 |

4.024271 |

38.80726 |

3.673461 |

9.923153 |

96.16605 |

|

2018 |

7.494572 |

4.034494 |

1.552319 |

3.341124 |

35.0576 |

5.30953 |

13.74027 |

95.37627 |

|

2019 |

9.150316 |

1.441306 |

2.350919 |